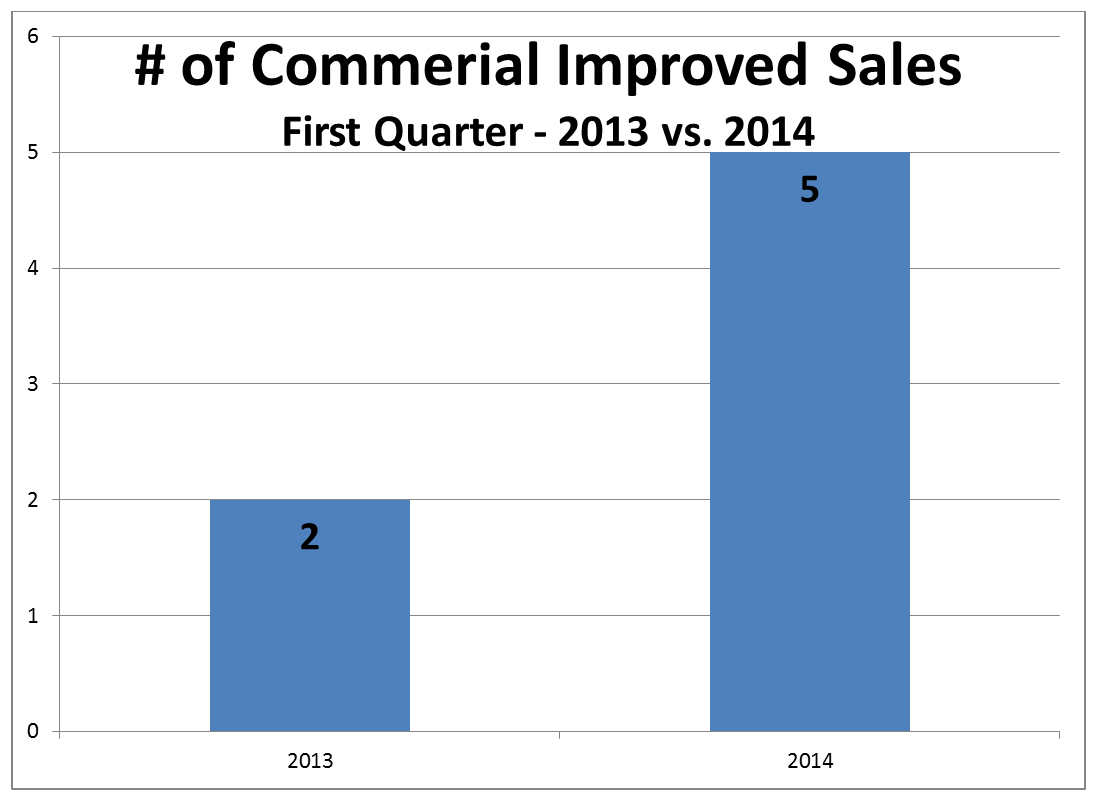

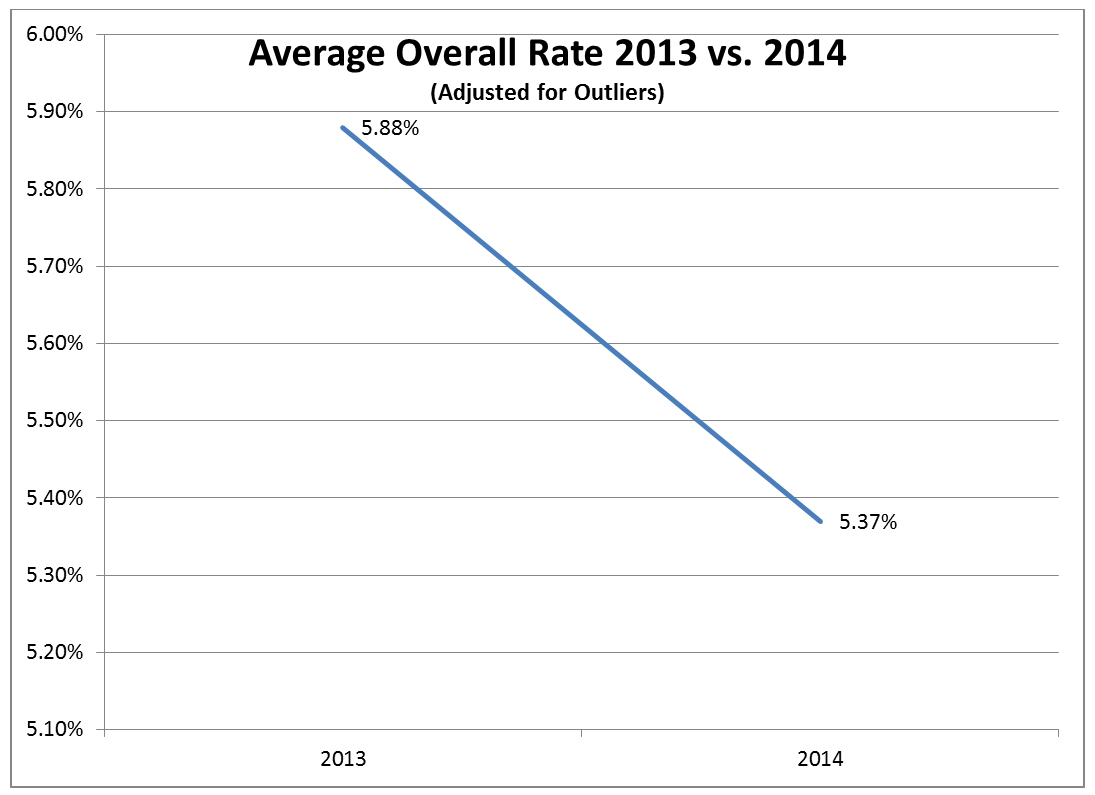

The first quarter of 2014 saw five commercial improved properties sell, with four out of five of these closings being for light industrial properties, including the over 17,000 square foot Wedco Building. Overall capitalization rates for these properties ranged from 5.06% to 8.76%, with the high end of this range being the result of an atypically motivated seller in one instance, and a sale out of foreclosure in the second. Excluding these sales the overall rates observed exhibited a relatively tight range, from 5.06% to 5.65%, with an average of 5.37%. This data is indicative of a more robust commercial real estate market existing in 2014 than was evident in 2013, when only two sales occurred in the first quarter. Those sales exhibited an average overall rate of 5.88%. This drop in overall rate equates to a nearly 9.5% increase in improved commercial income property. There were also two vacant land commercial sales in the first quarter of 2014, which is one less that was observed in 2013. One of these sales is located in the AC zoning district and was purchased at an over 50% premium from similarly-zoned property that sold the previous year. Admittedly, the difference between these lots location is thought to be contributory to the magnitude of this price differential but, nonetheless, it is an encouraging data point.

![]() Andrew Cornish | Broker

Andrew Cornish | Broker

PO Box 9467 | 155 E. Pearl Avenue, Suite 10

Jackson, WY 83002

(307) 733.8899 | (307) 413.7799 cell

Linkedin

Access to the most comprehensive sales database anywhere

from the leading brokerage and appraisal business in Teton County.

![]() Andrew Cornish MAI, SRA

Andrew Cornish MAI, SRA

www.rmappraisals.com

I was initially given pause last year during the course of a casual conversation when it was remarked that, “you can’t really find a decent lot in Teton County for less than $5,000,000.” My surprise at this comment was somewhat lessened when the definition of a “decent lot” was further classified as being three acres or larger, within 15-20 minutes of Teton Village and uniformly comprised newer high-end construction.

I was initially given pause last year during the course of a casual conversation when it was remarked that, “you can’t really find a decent lot in Teton County for less than $5,000,000.” My surprise at this comment was somewhat lessened when the definition of a “decent lot” was further classified as being three acres or larger, within 15-20 minutes of Teton Village and uniformly comprised newer high-end construction.